The uncomfortable number

Matt Greer

“Am I saving enough?”

This is a question even the most disciplined investors ask themselves from time to time. And while a financial plan can go a long way towards answering this question, there’s always the unknown unknowns we cannot factor in.

Educated investors understand the logic well enough. By putting money away today and letting it grow, we will enjoy the benefits later. While there’s no mystery around this concept, the big question becomes whether we are putting aside enough money for our “future self”, someone who feels like a complete stranger to us right now.

If you’re already saving, that’s great. But if it feels perfectly comfortable, there’s a reasonable chance it’s not enough.

In many cases, we’ve seen that the amount that actually builds real wealth is the amount that feels slightly uncomfortable on an ongoing basis.

The Negotiation You’re Always Having

Every financial decision you make is really a negotiation between two versions of yourself. While “present you” wants ease and comfort, “future you” needs you to stretch and make a little sacrifice.

We know from both research and practical experience that we naturally overvalue what feels good right now while discounting what we’ll need decades from now. It’s why the contribution amount that feels right often isn’t. We set it based on today’s comfort and desires rather than our future well-being.

The slightly uncomfortable savings amount is where these two versions of you meet in the middle. It’s the number where “present you” feels a genuine pinch. This may mean pausing before you pay for that holiday or making the deposit on a new car. Sometimes, discipline means saying no more often than you’d like.

That tension may be a sign that you are doing the real work of building wealth.

More Than A Number

The personal finance world loves percentages. Many investors will know the general advice to save 15%, and if you started late, maybe 20% of your net income.

But your life goes beyond rules of thumb, and while they are a brilliant way to get the average investor onto the right path, true financial planning should incorporate real numbers based on your own unique circumstances and goals.

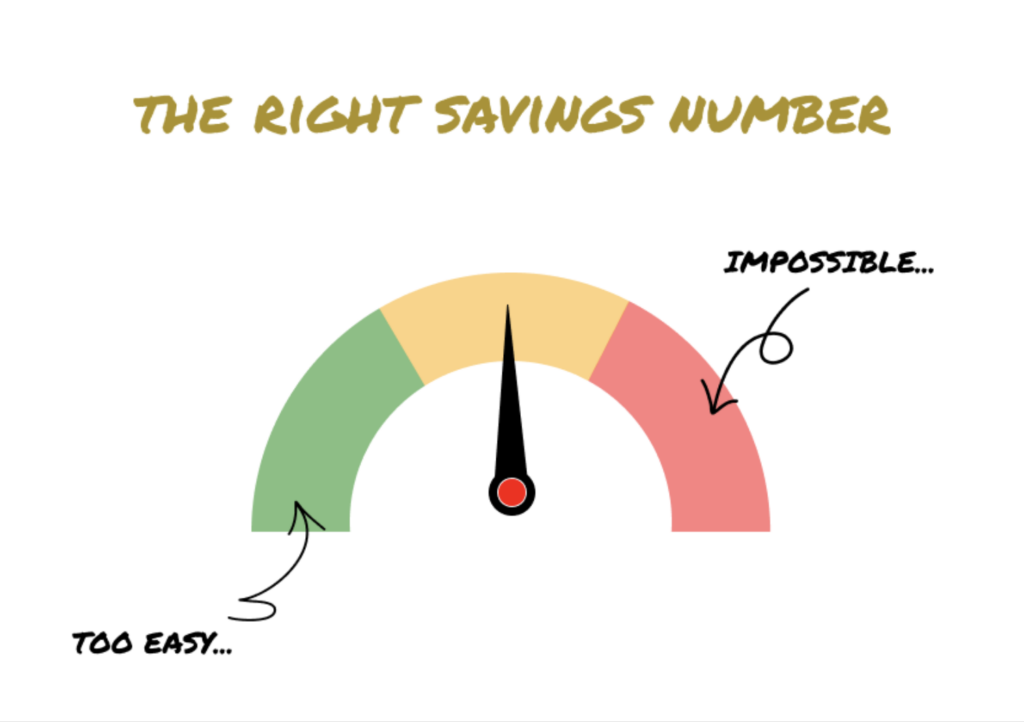

However, we think that this topic goes beyond numbers. Your correct savings number is better understood as a feeling. You need to be able to sustain it month after month, but it also requires intention and occasional sacrifice. That’s the sweet spot. If it feels easy, you’re probably selling your “future self” short. If it feels impossible, you’ll abandon ship at the first unexpected expense.

Somewhere in the middle, right between where it feels like a pinch and where it feels impossible, is most often the right answer.

We think this mental model carries over into other topics, too.

Your emergency fund should probably feel slightly larger than strictly necessary. Cutting back spending works best when there’s some friction to it. Even career moves that lead to higher earnings usually feel uncomfortable before they pay off.

An Ongoing Challenge

As life evolves, so should your number. Every pay increase is an opportunity to widen the gap between what you earn and what you spend, and annual nudges that push you gently back into that discomfort zone will keep your “future self” on track

In summary, being easy on your “present self” harms your “future self”. We encourage you to aim for some discomfort now so that you can enjoy significant comfort later. That’s the trade-off, but we think the sacrifice will be worth it in the long run.

Our job is to continually push you into this discomfort zone so that your “future self” can enjoy the comfort you crave.

Our reputation

I have peace of mind that we are on track to achieving what we want out of life. I feel we have our finances in order now and we are really making the most of what we have.

The process gave us tremendous peace of mind - knowing we have financial security and that any necessary advice and decisions are taken with the help of a professional.

Through the use of cashflow planning I have been able to get a greater handle on my income and expenditure and Paul is able to show me that I am on track to achieving my goals

We meet twice a year, but Darren is always on hand should I have any “financial ideas”, queries or problems. If it is not in his expertise, he has no hesitation in bringing in one of his considerably gifted team.

It is great to have an expert look after my finances and it gives me peace of mind to know that my retirement fund is being well looked after

We have been very impressed with Michael’s honest and personable approach to dealing with our finances and he has always gone out of his way to make sure we were happy.